Strategy

National Strategic Assessment 2020

This report sets out our latest assessment of the issues we face and the risks that gambling poses to consumers and the public

What do we know?

Gambling participation

Gambling is a popular activity in Great Britain. Our latest annual data shows that 24.7m adults in Great Britain participated in gambling in the last four weeks.

Gambling participation is not increasing. At an overall level, participation rates have remained stable in recent years. The latest annual data shows 47% of adults had gambled in the last four weeks, with rates consistently between 45-48% since 20151.

The most popular gambling activities by participation rates are:

| Activity | % Participation |

|---|---|

| National lottery draws | 30% |

| Other lotteries | 13% |

| Scratchcards | 10% |

When National Lottery products are excluded, our data show that 32% of adults (17.0 million) participated in other forms of gambling in the last four weeks. This rate has remained relatively stable over the last few years2.

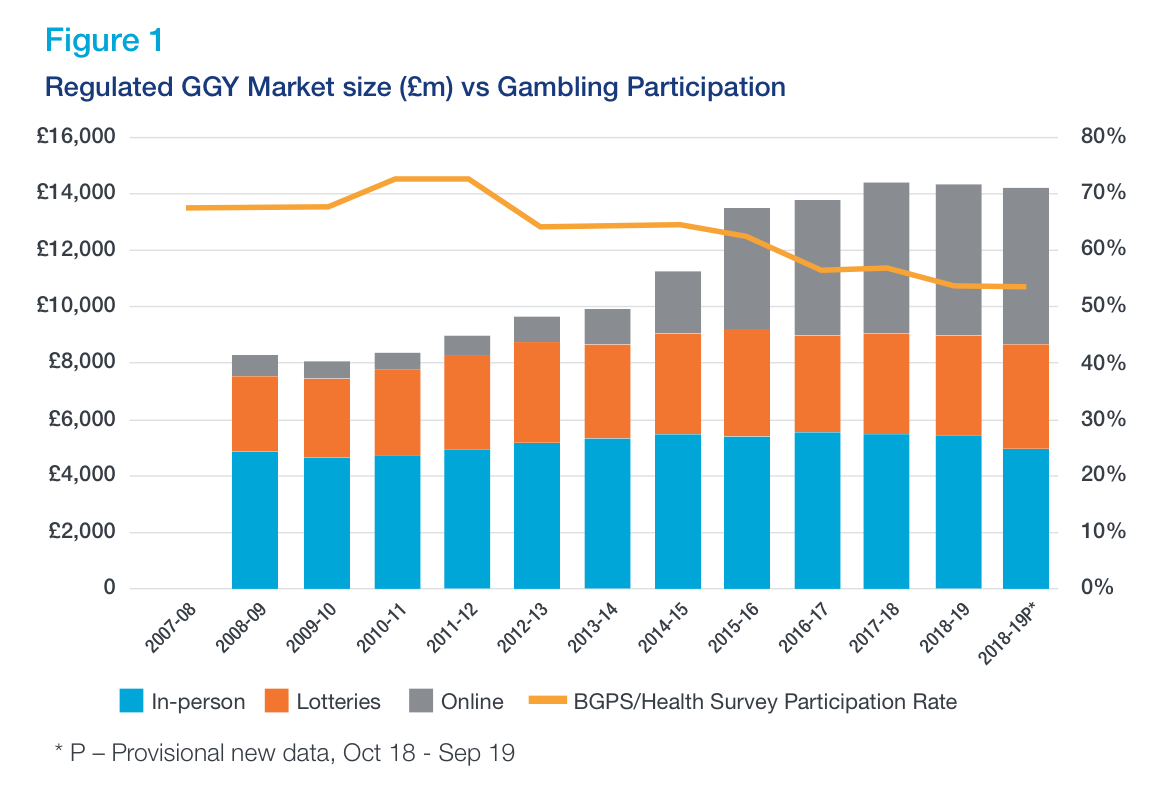

Figure 1 which shows a longer-term trend tracking participation in gambling in the last 12 months (rather than the last 4 weeks), shows a decrease in participation alongside the growth in industry gross gambling yield 3.

The Gambling Commission’s data shows that the increase in Gross Gambling Yield (GGY) has been driven by increases in participation and spending on online gambling.

This growth in online GGY was significantly impacted by the shift to point of consumption regulation in November 2014 4. The 2015/16 figures represent a better benchmark from which to assess changes in consumer behaviour, as that was the first full year the Commission collected the data directly.

Our data shows that online gambling has grown by 30% since 2015/16, compared with a 8% decline in premises based gambling.

In overall terms, the combination of lower levels of participation and increases in industry GGY means that average gambling loss per consumer has increased. We explore the risks posed by the increase in customer losses from certain products such as online slots in Chapter 3.

References

1Gambling participation in 2019 behaviour awareness and attitudes (PDF) (opens in new tab) Throughout this document, when using statistics from our quarterly telephone survey, we have drawn these from the most recent annual report published in February 2020 which covers the year to December 2019, and therefore predates the coronavirus (COVID-19) period. Please see Chapter 6 for more detail on our research during the coronavirus period.

2Gambling participation in 2019 behaviour awareness and attitudes (PDF) (opens in new tab)

3 GGY is effectively stakes minus prizes

4 Gambling (Licensing and Advertising) Act 2014

Key issues and risks Next section

Understanding why people gamble

Last updated: 25 July 2024

Show updates to this content

Following an audit corrected link formatting issues only.